Is it smarter to pay down a mortgage or invest? The answer depends on a range of factors.

Many borrowers don’t have the financial capacity to make additional repayments on their loans, especially during times when interest rates are rising.

However, some borrowers are in the position of having accumulated savings and regular surplus income that can potentially be used to make extra loan repayments. Others may receive extra income on an ad hoc basis, such as from a company bonus, sales commissions, gifts, or from other sources which also could be applied to debts.

Alternatively, instead of using extra income to make additional loan repayments, another option could be to invest the money in other assets.

Is one approach better than the other?

The answer to this question is highly complex, because among other things it really depends on one’s personal circumstances and financial goals, attitudes to risk and potential cash needs, the amount of debt outstanding and the overall cost of servicing it (interest charges and fees).

Reducing the amount owing on a loan will reduce monthly repayments, the interest charges on the outstanding balance and, most likely, the overall term of a loan.

On the other hand, investing additional funds into other areas can potentially offset the debt-servicing costs of a loan over time if the net returns from those investments are higher.

For example, if the average interest rate on a variable rate owner-occupied home loan over its term was 5%, while the net returns from an investment over the same period of time was 9%, then one could build a case that investing surplus funds may be a better path.

The 2023 Vanguard Index Chart shows that the Australian share market, measured by the S&P/ASX All Ordinaries Total Return Index, returned an average of 9.2% per annum over the 30-year period from 1 July 1993 to 30 June 2023.

It should be noted however that investment returns may end up being lower than the overall costs associated with a loan, and even negative, at different points in time.

Unfortunately, there is no crystal ball to predict future investment returns, let alone future interest rates.

There can also be tax considerations to take into account, such as the allowable negative gearing deductions available to many investment property owners. These can have a significant impact on the long-term investment returns from a property. Likewise, there may also be tax benefits to individuals with investments outside of property.

Investors also need to consider that investment returns may be subject to income tax and capital gains tax.

Doing the numbers

It is possible however, taking into account that past investment returns are not an indicator of future returns, and that historical interest rates are not a predictor of future rates, to use past data as a general reference point.

For the purpose of this exercise we’ve used the Reserve Bank of Australia’s (RBA’s) monthly lending rates data and the returns from a range of different investment asset classes.

The RBA’s November data shows the average standard owner-occupier variable home loan mortgage rate over the decade from October 2013 to October 2023, taking into account interest rate rises and falls, was 5.52%.

Using the 5.52% average mortgage rate, a borrower taking out a $400,000 loan in October 2013 would have paid out $142,185 in interest (approximately $1,185 per month) over 10 years.

So, hypothetically, what would have happened if they had received a $10,000 company bonus right at the start of their loan and chosen to apply it to their mortgage?

Based on the same 5.52% average mortgage rate, by reducing their mortgage to $390,000 they would have ended up paying out $138,631 in interest (approximately $1,155 per month) over 10 years. That’s an interest saving of $3,554 when compared with the interest on a $400,000 mortgage.

How would that have compared with different investment returns over the same period of time, from October 2013 to October 2023?

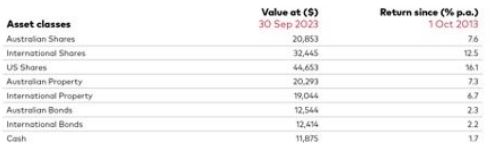

The Vanguard Digital Index Chart maps the compound returns achieved by different asset classes over time.

The table below shows the average annual compound returns from 1 October 2013 to 30 September 2023 based on a $10,000 initial investment and the reinvestment of all the income (company dividends or other income distributions) received.

On average, shares have achieved the strongest average annual investment returns over the past decade, followed by listed property securities.

Past performance is not a reliable indicator of future performance.

Sources: Vanguard, Andex Charts.

Note: The returns in the table above assume all investment income earned was reinvested and exclude investment fees, expenses, transaction costs and taxes. When calculating returns inflation has not been taken into account. All returns are quoted in Australian dollars. U.S. and International Shares returns are affected by exchange rate movements.

Taking the 7.6% average annual return from Australian shares as an example, a borrower paying a 5.52% mortgage interest rate could have been slightly ahead by investing $10,000 over 10 years (without factoring in potential taxes on earnings and investment costs payable). The case for investing over a $10,000 debt repayment was stronger for United States and international shares.

As noted, there are a range of things to consider based on one’s personal circumstances before deciding whether to pay down debt or to direct extra money into investments. There is no one-size fits all approach.

Investment returns can be volatile, and some asset classes can deliver low or negative returns. As such, depending on the mortgage interest rate being paid, borrowers may not be able to achieve an investment return that is high enough to compensate for the additional interest being paid.

If in doubt, our financial advisers can take into account all your specific characteristics and help define the best course of action.

SOURCE

The above material has been reprinted with the permission of Vanguard Investments Australia Ltd