Schedule a Chat

Contact Info

Suite 17.03, Level 17

20 Bond Street

Sydney NSW 2000

INSIGHTS WITH EVALESCO

TOPICS DISCUSSED

As of July 1, 2022, new rules will benefit retirees through contribution opportunities, tax breaks for home buyers, downsizers, and contribution opportunities for those earning less than $450 per month.

There are changes to super which take effect from 1 July 2022. The following are changes you should know about:

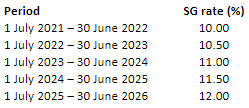

An increase in the Super Guarantee rate

The compulsory SG contributions employers pay to employees will increase to 10.5% from 10%. The SG contribution rate will continue to increase by 0.5% until it reaches 12% in 2025. The table below shows the contribution rates that will apply in the coming years.

Removal of $450 monthly income threshold

The monthly minimum wage threshold of $450 for employees to qualify for SG payments will be removed from 1 July 2022. This measure primarily assists low-income earners to have employer contributions paid to super boosting their retirement savings. Employers will be required to pay SG contributions to their employees 18 years and older, even when the employee earns less than $450 each month.

Abolishing the work test for people aged between 67 and 74

From 1 July 2022, members under 75 years of age will be able to make or receive personal contributions and salary sacrificed contributions without meeting the work test, subject to existing contribution cap limits. They may also be able use the bring forward rule. However, those aged 67 to 74 will need to meet the work test if they wish to claim a personal super deduction for their contribution.

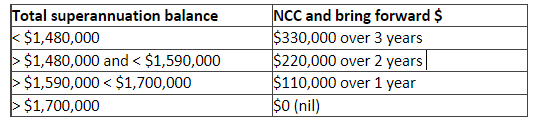

Increasing the bring forward non-concessional contribution rule

For those aged 67 to 74, the bring forward non-concessional contribution rule will be increased.

The non-concessional contribution cap is $110,000 for the 2021-22 year. The 2020-21 NCC cap was $100,000.

For the 2021-22 year, members aged under 67 have an option to contribute up to $330,000 ove a three-year period, depending on their total superannuation balance (TSB).

From July 1, 2022, members aged under 75 (up from age 67) will have now have an option to contribute up to $330,000 over a three-year period, depending on their total superannuation balance (TSB).

The TSB rule is as follows for 2021-22 onwards:

New age threshold for downsizers

If you have reached the eligible age, you may be able to contribute up to $300,000 from the proceeds of the sale (or part sale) of your home into your super fund.

From 1 July 2022 the eligible age is 60 years old or older. Prior to this it is 65 years old or older.

Other eligibility criteria will apply.

First Home Super Saver (FHSS) Scheme

From 1 July 2022, the amount of eligible contributions that can count towards your maximum releasable amount across all years will increase from $30,000 to $50,000. The amount of eligible contributions that can count towards your FHSS maximum releasable amount for each financial year will remain at $15,000.

The FHSS scheme allows you to save money for your first home inside your super fund. This will help first home buyers save faster with the concessional tax treatment of superannuation.

To watch the webinar on these changes click here

SHARE OUR INSIGHTS

Share on Facebook

Share on Email

Share on Linkedin

NEWSLETTER

Evalesco Financial Services Level 17, 20 Bond Street Sydney NSW 2000

Phone: (02) 9232 6800

The information provided on and made available through this website does not constitute financial product advice. The information is of a general nature only and does not take into account your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice. We recommend that you obtain your own independent professional advice before making any decision in relation to your particular requirements or circumstances. Evalesco Financial Services do not warrant the accuracy, completeness or currency of the information provided on and made available through this website. Past performance of any product discussed on this website is not indicative of future performance. Copyright © 2019 Evalesco Financial Services. All rights reserved